Insights & Opinions

More Insights & Opinions

Rather than treating agentic AI as the next fashionable label, Wesley Wuyts of SAS framed it as a response to a practical gap that banks have been wrestling with for years

Reflecting on the future of the banking industry in the run up to our flagship conference on May 28

A recap of a roundtable discussion held with a group of senior banking executives under the Chatham House Rule, which surfaced a striking degree of candour and consensus about both the transformative potential of Agentic AI and the very real challenges that lie ahead

The question is no longer whether banks can deploy generative AI, it is whether they can build systems that can act.

As instant payments become the norm across Europe, banks face a tougher balancing act between speed, convenience and fraud prevention - why Verification of Payee is helping but not solving everything, and why the future of fraud prevention will depend on layered controls, better collaboration and smarter use of friction.

Dharmesh Mistry's latest research into what he calls the "Quanvergence" suggests that we are moving past the era of digital delivery into an era of deep, structural change driven by four intersecting forces: Quantum computing, Digital Twins, Agentic AI, and Tokenisation.

ClearBank's recent MiCAR notification does not represent a strategic pivot towards crypto, nor does it suggest a belief in a wholesale transition to new rails. It is an extension of an existing role.

We love to talk about technology developments and opportunities, but what often remains underexposed is the more difficult question: how do these innovations translate into something meaningful, usable, and trusted by customers?

Recent interactions with industry experts have revealed that the banking industry is not aligned on the definition of "Agentic AI". When two organisations assert they are investing in Agentic AI but have different interpretations, they aren't simply on separate paths; they are addressing different problems.

Tokenised assets and digital currencies are hot topics in the banking and financial services world right now and that also makes them hot topics in the world of fraud and scams.

The more I speak to bankers, technologists and transformation leaders, the more I come around to thinking that the story of AI in banking is not that machines are becoming more capable, but that people are becoming more essential.

Quantum computing challenges the assumption that our security technology keeps our digital communication and authentication safe. We explored the urgency (or not) for banks of post-quantum cryptography in a round table.

Tokenisation does not need to replace existing systems to become relevant. It only needs to prove incrementally superior to what we knew yesterday.

Fraudsters move fast. Regulation, controls and customer education eventually catch up and then criminals change tactics again. That constant cat-and-mouse dynamic was a recurring theme in my conversation with Remy Knecht, Head of Anti-Fraud Services at Isabel.

Fraud and scams are rising across Europe, and the view of Frédéric Lebeau, Founder of Datavillage.ai, is that the type of fraud growing fastest matters as much as the volume

Loading more...

Jimmy Donaldson aka "MrBeast" bought Step, a fintech app with a noble mission to strengthen young people’s financial capabilities.

We explore what it takes for banks to remain meaningful in customers’ lives as technology accelerates, fraud evolves, and expectations keep shifting.

Rik explores the conversations he is having today about his book, exploring the same idea from the outside in: relevance, trust, and judgment under pressure. It is the same story, but seen from a different angle.

Covering unanswered questions following our webinar on fraud and scams in Benelux banking with Jorij Abraham, Managing Director of The Global Anti-Scam Alliance.

A summary of the key points raised during our webinar with Jorij Abraham, Managing Director, Global Anti-Scam Alliance on The Global State of Scams with highlights from Belgium and the Netherlands

We look at the 2026 banking landscape through the lens of recent reports and our own upcoming events

Deepak Pandey, Vice President of Technology at Backbase, cuts through the noise and lays out what it actually takes to turn AI into a real growth engine, not just another bolt-on to old architectures.

Nickel has expanded rapidly across France, not with a digital-only strategy as most neobanks, but with a conscious choice to rely on human contact

In conversation with Sofia Pogrebynska, IT & Cloud Officer at PayPal, it turns out that the biggest shift in cybersecurity today has less to do with technology and far more to do with how organisations behave and operate.

Bankers know that know they must evolve to survive, yet they operate within structures explicitly engineered to prevent that evolution - this is the essence of The Innovation Paradox.

As generative AI tools race ahead, many banks are left wondering how to balance innovation with governance, ethics, and risk. The key takeaway: the stakes are high, but with the right approach, responsible AI can become a competitive advantage, not a compliance headache.

Our speakers shared how they are rethinking assumptions, reimagining customer relationships, and reconsidering the role banks should play in society.

The real recipe for success in open finance is about contextualising innovation to local ecosystems while pushing for global interoperability.

Revolut is no longer just a travel card in Belgium. With Belgian bank accounts and instant savings with daily interest, it is quietly becoming a serious contender. Here’s what that means for Belgian banks.

Banking faces a quantum future. Rik Coeckelbergs reflects on insights from IBM, BBVA, and CWI at SIBOS — and why preparation starts long before production.

Loading more...

A deep dive into 2055’s consumer finance landscape: AI credit models, embedded finance, tokenisation, and the shift from super apps to modular platforms.

During the “The Psychology of Online Fraud” session delivered by Paul Maskall at Open Banking Expo, Rik discovered that fraudsters and marketing people use the same tactics with different intent!

Today, blockchain is shedding its rebellious reputation and becoming one of the major civic technologies of our time, turning transparency into policy, accountability into code, and collaboration into design.

From how communities think about obligation and reciprocity to whether trust sits in credit scores or social ties, payments and money are never culturally neutral. If banks want AI that works globally, they must design for local meaning.

During SIBOS, Deutsche Bank and TechQuartier hosted the FiDA Data Studio at the EintrachtLab in Frankfurt to explore how Open Finance, structured data, and AI-powered services can unlock customer-focused, scalable innovation across Europe’s financial system.

Belgian banks face rising scams, instant payment risks, and liability shifts. Why collaboration 2.0 is vital for fraud prevention in 2025

We invited six experts to share their unfiltered vision of the future of payments in 2030 and beyond at The Banking Scene BBQ Night - read on for their predictions and insights

The future of payments will be shaped by three key forces: Trust, Technology, and Transformation, which will help create a world where payments are not only easy and safe but accessible to everyone.

Can banks change your money habits? BBVA’s Coach and ABN AMRO’s BUUT show how digital coaching is redefining financial wellbeing from kids to adults.

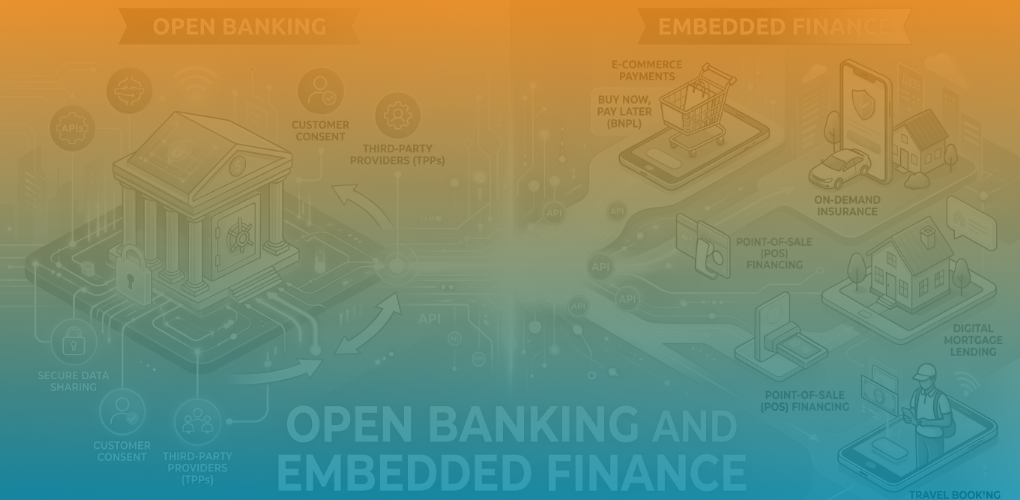

As layers of technology, coupled with open banking and embedded finance, threaten to push bank brands further and further into the background, how will they remain relevant in tomorrow’s world?

Revolut launches daily interest payouts in Belgium. What does this mean for savings expectations, incumbents, and the future of digital banking?

As third-party providers become indispensable to delivering modern banking experiences, the concept of identity and access management (IAM) is undergoing a fundamental shift.

I missed the kickoff of the Belgian Football Jupiler Pro League while hiking in the Swiss Alps and I blamed my bank - find out why and what lessons I think banks can learn from my experience.

The banking industry is on the cusp of a profound transformation, not only from banks using AI, but from their customers using AI (bots) to navigate their financial lives.

Banks are shifting from traditional, product-led institutions to dynamic, service-oriented ecosystems, designed not just around technology, but around people.

Loading more...

As CBDCs move from theory to reality, particularly in Europe, a panel of experts explored the evolving impact of Central Bank Digital Currencies (CBDCs) on both wholesale and retail payment landscapes

Quantum computing, once the realm of science fiction, is rapidly transitioning from theoretical possibility to technological reality - is the banking world ready for it?

A discussion on how Belgian banks can reconcile compliance obligations with the financial inclusion of legally recognised sex workers, with Belfius, UTSOPI, moderated by Aliya Shibli from "The Banker" by FT

A recap of TBSCONF25BXL’s panel on how retail-focused payment regulations often miss the mark in corporate banking—and what needs to change.

According to Signicat’s Battle in the Dark report, 74% of businesses believe they are “winning” the fight against identity fraud

A exploration of whether banks are truly delivering on their purpose, values, and customer experience promises—through the lens of ethos, logos, and pathos.

Payments orchestration has moved from innovation to expectation; it’s the silent engine driving global payment strategies

At the core of Monzo’s purpose is a deceptively simple insight: most people have a troubled, even avoidant, relationship with money.

Reality and digital are being merged through deepfakes and AI, introducing new societal challenges to the already fragile balance between digital convenience and optimal services - how is this impacting Financial Services today?

From operational efficiency and internal productivity to customer engagement and strategic governance, the message was loud and clear: GenAI is no longer a playground for pilots, it's a catalyst for real transformation.

The future of banking will be shaped less by technology itself and more by the way banks integrate intelligence, artificial and human, into their core.

The European Commission released a non-paper on the simplification of the Financial Information Data Access (FiDA) Regulation on May 16 - does this address industry concerns?

Across the sector, banks are shifting from traditional, product-led institutions to dynamic, service-oriented ecosystems, designed not just around technology, but around people.

As cross-border spending gains traction in post-pandemic Europe, the Japanese payment brand JCB is quietly reinforcing its foothold across the continent.

In today’s fast-paced digital economy, chargeback fraud has quietly evolved into one of the most pressing challenges for merchants, financial institutions, and payment service providers.

Loading more...

At MPE 2025, the narrative was clear: the payments industry is converging, but not just across rails and channels.

While the types of fraud may not have dramatically changed over the last decade, the methods used to carry them out and the tools required to combat them have evolved rapidly.

Digital Identity is key to building the capability to withstand new attack vectors and protect trust In an era of unprecedented digital transformation and rising cyber-enabled financial crime.

One of the newest threats identified by XTN Cognitive Security is what Guido calls the “Shell Game Malware” attack.

Artificial Intelligence (AI), and more recently Generative AI (GenAI), is no longer just a buzzword. It's evolving into a set of practical tools with real business value

Many players benchmark their expectations on what they see happening in the U.S. But that’s often a mistake!

In a digital-first financial world, fraudsters are evolving faster than ever. Yet for Baptiste Védère, Chief Risk Officer at Santander Consumer Bank in Belgium, staying ahead of them starts with a strong foundation: cybersecurity, risk culture, and industry collaboration

Two powerful narratives converged at The Banking Scene Conference Amsterdam: the evolution of financial data access (FiDA) as a regulatory force and the rising strategic importance of identity in the age of fraud, AI, and hyper-personalisation.

We explore the evolving fraud landscape, the unique challenges fraud prevention teams face, and how Adyen’s vast dataset provides a competitive edge in keeping merchants and customers safe.

The rapid evolution of digital banking and increasingly sophisticated fraud tactics have forced financial institutions to rethink how they approach financial crime.

BNP Paribas is making significant strides in applying artificial intelligence (AI) to streamline operations, enhance customer interactions, and optimise risk management.

Banks worldwide are grappling with balancing legacy systems with new technology and meeting the innovation expectations of increasingly digital customers.

Modernisation in banking is an ongoing and often contentious topic, as our round table dinner discussions held with industry leaders revealed the challenges, opportunities and the road ahead

The Financial Information Data Access (FiDA) regulation remains a highly debated initiative in the European financial landscape

The future of banking will not be built in isolation. It will be forged through collaboration, trust, and a commitment to something greater than profit.

Loading more...

Leda Glyptis delivered a compelling keynote at The Banking Scene Conference Luxembourg based on her new book which investigates whether success in banking transformation follows repeatable patterns.

Since 2022, the industry acted reactively to every change in its path during unprecedented times, and transformed into a period of introspection, growth, redefinition and initiative

Like Frodo and his companions embarking on their perilous journey to Mordor, the Wealthtech industry faces a challenging quest: to harness the power of FiDA for innovation and collaboration while avoiding the chaos of mistrust and fragmentation.

Following the centuries old tradition of Belgian children, I write a 2025 New Year Letter to the Banking Industry, sharing my wishes for what will come about.

Fraud is no longer an isolated issue—it’s a growing crisis affecting businesses, consumers, and the integrity of our financial systems

Our round table dinner session in Amsterdam with asset and pension fund managers revealed interesting insights regarding financial services sustainability regulation and AI's role in helping to shape a greener future.

Wero embodies EPI's ambition to create a unified, seamless, and secure digital payment solution for Europe by integrating features such as instant account-to-account transfers, QR code payments, and cross-border functionality

The Banking Scene Art Night 2024 delved deeply into how money flows in our financial ecosystem and the possibilities of transformative change.

The SEPA Payment Account Access (SPAA) scheme is set to reshape the European payments ecosystem, offering banks and fintechs a chance to thrive in an era of open banking.

At a recent roundtable dinner held in Luxembourg, we gathered a small group of industry leaders to share insights on the structural, cultural, and psychological hurdles they face in embracing change and innovation in wealth management

Belgium's payments landscape has transformed in recent years and now includes a larger European push towards a unified payment solution via EPI (European Payments Initiative)

The shift from open banking to open finance is happening globally, but the pace and priorities differ greatly by region.

Financial data access has emerged as a pivotal factor driving innovation, competition, and enhanced customer experiences.

Financial institutions need to consider several key factors in preparation for the upcoming introduction of the European Digital Identity Wallet (EUDI).

The banking sector has seen a surge in mergers and acquisitions in recent years, with several notable takeovers highlighting the consolidation trend.

Loading more...

Transforming the Rules of Engagement in Times of Digital Banking, AI and GenAI

If banks want to be remembered for more than cash machines, it is time to review thier measurements of success

Strategies for future-proof payments must address technological advancements, customer demands, and the increasing role of security and compliance.

Looking through the lens of strategic foresight to the year 2525 may not sound useful, but it can help challenge assumptions that will shape your thinkiing today.

We all have dreams and most of them need money in order to realise them. KBC and Doconomy have teamed up to help KBC customers visualise their dreams and make them real

Consumers expect frictionless payments until the time they are thankful for a bit of friction that helps prevent fraud - but how sustainable is this to continue in the long term?

Much like a caterpillar evolving into a butterfly, banks are undergoing an internal metamorphosis, reshaping their core structures, strategies, and cultures to thrive in a rapidly changing environment.

We debate The Evolving Relationship Between Banks and Fintech Companies and conclude that banks view fintech companies more as friend than foe.

Visa's Innovations help take the sting out of holiday spending and give you extra peace of mind when you travel

Central Bank Digital Currencies (CBDCs) remain a divisive topic in the financial sector, generating a mix of excitement and concern.

Chilosi envisions a future where all 4 primary models for cross-border payments coexist harmoniously and predicts that transactions in the future are probably going to have to go into multiple networks.

AI has rapidly become a transformative force in the banking sector, offering numerous opportunities while also presenting significant ethical, environmental, and regulatory challenges.

Jean-Baptiste Beaux of Comarch shared that by leading in customer engagement, wealth management firms will also lead in Customer Lifetime Value (CLV)

The fastest heist in history took just 2 minutes to steal 625 million USD, but how the hackers gained critical info to enable the heist might surprise you

Crown Agents Bank's core strength lies in its deep focus on payments and FX in emerging markets.

Loading more...

Euroclear's current view of Generative AI is that it is an augmentation to human capability, not a replacement of it. Their legal team are pioneering the first use case.

Traditional Know Your Customer (KYC) processes are no longer sufficient. Continuous identity verification and real-time adaptive access decisioning throughout the customer journey is essential to detect and prevent fraud in real-time.

Karin Van Hoecke of KBC Bank and Insurance shares he thoughts and insights on the use of Generative AI, and concludes that it should rather be viewed as an incremental improvement to existing AI, not as a standalone technology.

Recognising that cards are not the preferred payment method in many countries, payabl. expanded its services to include local payment methods.

There is an undercurrent of enthusiasm among employees about AI's potential, in spite of Rabobank's conservative start.

vdk bank created a unique triple-sided coin representing the customer, the community and the planet, to encourage discussions around the choices people should make when choosing a bank.

Thought leaders from Commerzbank, De Volksbank and nCino share their insights on the key points to consider when implementing AI in banking and financial services.

Peter Surek, Chief Executive Officer of Erste Finance Holding, shares how one of the largest financial institutions in Central and Eastern Europe balances its social and commercial goals, demonstrating what can be done by banks.

Breaking up with your bank of 27 years is surprisingly simple and hurts the bank far more than the customer

As we increasingly rely on digital forms of money and payments, the resilience and availability of banking infrastructure and services becomes increasingly important.

ING's approach is not to compete with big tech, but rather to evaluate how they can securely use the existing solutions in a responsible and reliable way.

The early use cases for GenAI identified by Christophe Atten at Spuerkeess focus on making the lives of employees better - basically giving them superpowers

Generative AI Use Cases and Opportunities in Banking: Keeping a Human in the Loop is essential for now, but may not be forever.

Big banks can't start over from scratch, but by reducing the complexity of silos through progressive modernisation, they can transform the rules of engagement from within.

Every bank operates in a unique environment with specific business models and cultures, which provides the context for the ethos of the bank.

Loading more...

Fully embracing Embedded Finance requires you to focus your attention on a much broader group of stakeholders than ever before. We dig into the implications.

The conversations in wealth management and private banking are changing. There is a shift towards more meaningful conversations about wealth, its purpose, and its legacy.

We conclude our interview with Eelco Dubbeling of the Dutch Banking Association by exploring diversity, inclusion, regulation and more.

How does "The Banker's Oath" impact the culture and ethos of a bank, and is it even necessary given young people's attitudes towards working in financial services today?

Could artificial intelligence finally help banks replace "my father's banak manager" that I've been searching for?

Our panellists at TBSCONF24LUX collectively acknowledged the critical importance of ESG in the banking sector. They highlighted the challenges posed by complex regulations, the imperative of education, and the development of a positive narrative as key to engaging employees and customers.

This interview has got me wondering once again to what extent the business model of a bank determines its definition of ethos, and how that impacts its daily operations.

Customer centricity is directly impacted by the degree to which a bank has undergone a complete digital transformation

Regulation is often thought of as a "necessary evil". It can be both an enabler of opportunities and a barrier between banks and their clients.

To what extent can we change the role of the bank within society and what is expected from these banks?

Who better to speak to when writing a book about Ethos and Ethics than an Ethicist

Becoming a Green Bank has progressed beyond simply removing paper from the processes to "sustainability by design".

Customer centricity is the key to winning back the trust of customers in banking, and it's all about finding the right balance in the Holy Trinity.

AI has dominated the news headlines over the last year - how will artificial intelligence impact the world of wealth management?

Martin Rohner, Executive Director at Global Alliance for Banking on Values challenges every bank to ask itself: what is my calling as a social institution, and where can I have an impact?

Loading more...

As Belgium’s most innovative bank and an example for banks worldwide, KBC looks at embedded finance in a somehow unique way

The battle between the credit union and mutual banking sector versus the big incumbents has parallels with the biblical story of David and Goliath - but who will win in the end?

Do you know what happened in the aftermath of the Global Financial Crisis and why there are 3 big international Greek companies in the software business of non-performing loans?

With the ISO20022 compliance deadline looming on the horizon, get up to speed on the impact and benefits to banks.

Michael Anseeuw, CEO & Chairman of the Executive Board, BNP Paribas Fortis, shares his advice on how to change the narrative of banking for the better

Digital transformation has been all about efficiency gains for too long. We learned how focussing on being effective is empathetic by design.

Do you know what happened with the FX Mortgage Loans in the Polish market and why Polish Banks are facing a $25 billion hit on the case?

Niccolo Polli delivered a very insightful and entertaining keynote at The Banking Scene Conference 2023 Brussels using the timeline of how Hollywood has portrayed banks to demonstrate how public perception has developed over time.

Could the highly skilled back office staff be leveraged to increase bank profitability through cross-selling? Would they want to?

"It’s all about being there where our clients are, on the platforms that our clients love, in the moments that matter to them." Find out how Rabobank brings this statement to life!

What does Ethos in Banking mean to you? Rik shares his understanding of the Rhetoric Triangle and what Ethos in Banking means to him in this context

How can incumbent banks showcase the opportunities that APIs could offer, to business people in order to stretch their imagination and stimulate innovative thinking?

Banking-As-A-Service, Software-As-A-Service, Infrastructure-As-A-Service, how do you select the right model for your business to maximise the benefits?

Rik shares with us the start of his journey to write a book on "A New Ethos in Banking – Embracing Values and Ethics for a Meaningful Transformation" and invites you to join as he shares his insights along the way.

Rik's reflections on the Future of Money following on from the panels and discussions at The Banking Scene Payments BBQ

Loading more...

Digitising the business back end is no longer a luxury; it's necessary to stay competitive and relevant in today's business landscape

Andrew's impressions on a recent Future of Money discussion featuring CBDCs, Metaverse, Star Trek, Tin Tin and much more

Often ignored in the embedded finance journey and debates are the challenge of offering these services. We spoke about that with OpenPayd's Barry O'Sullivan.

Financial institutions have many ways to reduce their carbon footprint, with immediate effect on cost reduction, like Green Coding, energy efficient data centers...

Early Wage Access and Earned Wage Access are completely different, their impact on financial well-being is the biggest difference

There is not digital transformation without integrating the back and middle office. What are the latest trends in that respect?

Read Rik Coeckelbergs's takeaways from PSD3 and Payment Services Regulation, the Open Finance Framework and the Single Currency Package

Process Mining: extract insights from existing data logs, map out all possible process flows, identify weaknesses and automation opportunities, and continuously monitor process performance for operational excellence and compliance.

Legacy creates confidence and trust, but comes with a cost. When and how can banks replace this trusted infrastructure? Episode Six works with progressively modernizing

How does Comarch tackle the desire of global scale efficiency with local customer centricity of their financial services clients?

Crown Agents Bank is in full expansion, we spoke with them at Money 20/20 Europe about their past, present and future

Is CBDC the right answer in a post-cash era for Central Bank to keep playing their supervisory role? Read what we learned from Yoav Soffer

We spoke a lot about open banking and PSD2 at #TBSCONF23BXL, including in a panel with Andreas Lennevi, Mendix. We continued the conversation afterwards.

The Banking Scene Attended Money 20/20 Europe on 6-8 June and this were the learnings

Ecosystem is a term often abused. Not in the case of Setle though. Learn how they built a network of data points to improve people's living journey in renovation at KBC and other financial institutions

Loading more...

Bitpanda is a precious fintech player in crypto space. Find out how they transform investment services and financial services at large.

Discussing the book "Banker Like US - Dispatches from an Industry in Transition" from Leda Glyptis on the challenge of transformation and diversity in banking

We spoke with Guus Loomans, Charity Manager at Rabobank about his exciting job and the tremendous impact they have on their clients and on society

What can we learn from SVB and Credit Suisse? Should banks rethink resilience? How important is technology and regtech in that exercise?

Read the results of a study by Dynafin with Solvay Business School of the maturity level of Belgian banks and FIs on the ESG risk framework implementation.

Rienk Franken's experience with Payday at ABN AMRO and extensive knowlegde on the gig economy gave me a much more holistic view on financial well-being

We spoke to Benoit Ouinas from Netcetera for a better understanding about the latest UX trends in card payments

After the decision that NewB would lose its banking license, they partnered with vdk bank for existence, and to fulfil their sustainability and ESG agenda

Mendix, one of our corporate members actively contributes to a better financial world with their low-code technology enabling the business to drive change

ISO 20022 is an open global standard for financial information. But why does it take decades for a global adoption?

We invited Peter Surek to talk about Erste Group's Social Banking Initiatives like FLiP, Zweite Sparkassen, Erste Social Finance Holding and much more

What is a Digital Asset Bank? What makes it different from digital wallets and cryptowallets or other blockchain technologies?

Sepa Payment Account Access it a new scheme building on PSD2 with Premium APIs to supercharge Open Banking

Financial inclusion, European sovereignty and innovation are the main drivers for Europe to develop a CBDC

What is it like to build and sell a regtech/fintech company in 5 years? We asked entrepreneur Klaas Van Imschoot, co-founder of b-Fine

Loading more...

What does it mean to transform a bank into a self-organisation? We asked Klaas Ariaans of ABN AMRO what his lessons learned are after implementing this philosophy 4 years ago

We spoke wit Mark Aldred, VP of International Sales at Auriga about banks, their branches and the impact of technology on the onmichannel customer experience (CX)

Early Wage Access can make a world of difference, if implemented correctly and with the right mindset, like Scudi and Rie Sordo are doing

With Catherine Bourin and Julien Froumouth, we discussed a recent survey highlighting the need for more financial education on the sustainable finance agenda

The European Commission recently issued a now proposal to speed up the process of making instant payments the new normal. What does this mean for the banking and payments industry?

Composable Banking of Mambu explains how you can select best-of-breed solutions around your core and build the bank you want to be, like Lego blocks

Learn how ROOV made the shift to B2B, grasping the opportunities of Open Banking and PSD2 to actively support the fight against poverty

12 months after his first visit, we invited Morgan Wirtz again to share us his journey of launching the bank Rise

We discussed the key learnings of Fincog's recent study on Banking for Tomorrow with Jeroen de Bel, Founder of Fincog and Branko Greganovic, of NLB

The first new clearing bank in the UK in 250 years, ClearBank is set to transform the payments industry with embedded banking and clearing services

Digital exclusion is a growing problem in Belgium. We discussed the latest statistics with Linde Verheyden of BNP Paribas Fortis and Ilse Mariën of Cabinet Bart Somers

DORA, Digital Operational Resilience Act it coming. How will it impact the way organisations communicate? Will it make negotiations easier?

We learned from Roland van der Vorst, Head of Innovation Rabobank about the importance of cooperative thinking in a global food revolution

Loading more...

With 8 executives we discussed the opportunities to balance the P&L in payments

With a delay of 1,5 years, the EC is now ready to review PSD2. What does this mean? We spoke to Febelfin and ESBG

At Money2020 Europe, we asked Jan-Willem van der Schoot about Mastercard's new strategic positioning of Debit Mastercard, Click-to-Pay and tokenisation

We asked Glen Fernandes of Euroclear to explain how their partnership with Fnality may disrupt capital markets

ClearBank is unique in its clearing, accounts, and embedded finance offering, we spoke to their CEO Charles McManus

Jo Coutuer is CDO at BNP Paribas Fortis for 6 years now, we asked him for his lessons learned to build a data-driven bank

The role of process mining in achieving operational excellence & accelerating digital transformation by Dynafin Consulting, proud partner of SOFTWARE AG

Money20/20 Europe felt different for me this year, this is why

Read how global banking authority Paolo Sironi believes the platform economie will transform banking as we know it

We discussed with Bernard Nicolay, Academic Director at Solvay Business School how he looks at the future of money

We cannot talk about financial inclusion and exclusion without looking at digital inclusion

How can banks balance the change that comes with the new way of working and the war for talent? We spoke to Jean-Philippe Thirion of TriFinance, Business Unit Leader Financial Institutions

Are banks really setting the right priorities in product development? We spoke with Tiina Laukkonen of Amazon about how they look at innovations in corporate payments.

Spuerkeess used blockchain technology to disrupt their student loan processes. Read here how they did this, why they did so and how successful it is

Learn how Axa Bank and Crelan transformed their performance management, becoming true business partners through Anaplan's connected planning

Loading more...

We spoke with Sandra Phlippen, Chief Economist at ABN AMRO about the impact of the Russie-Ukraine conflict on the banking industry and sustainability

We invited Discai CEO Fabrice Deprez for a chat on KBC Banks's recent BankTech initiative in their fight against financial crime

With Achim Thienel, of Finastra, we investigated the impact of cloud on banking and how it accelerates digital innovation

We asked Joris Krijger, AI&Ethics Officer at De Volksbank how to deal with AI, data, ML in an ethical way

Do we need digital cash like CBDC, Central Bank Digital Currencies? What value do they bring? And how do they compare to crypto?

What is Greenwashing and how big is the issue in financial services? It is something that can easily be stopped?

With new societal shifts, ESG, Ukraine war, inclusion... come new challenges that required a new way of banking

What's the buzz about niche banking, also known as affinity banking? A USP beyond banking, clear purpose and identification with the community

What's the added value for artists having their art linked to an NFT? How will the Metaverse impact our mental rest? We spoke to Jil Haberstig

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry, including Nasir Zubairi of the LHoFT

We spoke to Katrien Dewijngaert, GM Stratey and Transformation at KBC about KATE their AI driven virtual assistant

We invited Madeleine Debney, COO and Co-Founder of financial wellness platform Otto to talk about financial stress, financial wellness and wellbeing

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry, including Jonathan Prince of Finologee

SurePay joined us to explain the value of IBAN-Name Check in fraud prevention for banks as a tool to confirm the name of the payee

Bank Carige rolls out its first fully-digital branch with Auriga

Loading more...

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Sociéré Générale also contributed.

Read how Rabobank is influencing the Netherland's living conditions, though sustainable finance and making houses more accessible

AI and analytics are transforming banking and financial services, read from these learnings with Tableau, SWIFT and ABN AMRO how to reach the full potential

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Eric Mouilleron was one of the international contributors

Purpose and sustainability are the foundations of Triodos Bank, we asked Daan Vandevelde, Director Retail Banking how he looks at Banking for Good

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Angela Nickel, CEO of COMO Global was one of them

The RegTechBlackBook was Koen's first big project, now he launched The Sequel, a bundle full of insights and interpretations of regtech influencers worldwide

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Christophe Bourbier was one of the international contributors

Virtual Cards in B2B e-commerce help companies overcome some of their payments challenges, according to Matthijs Koorn, Research Director Payments at MGI Research

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Nicolas Gerard, executive of State Street Bank was one of them.

Tim Dierckxsens co-founded Venly with the ambition to make blockchain, virtual crypto wallets and NFT management accessible through a single API. What is his vision on money?

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Pascal Morosini, CEO of i-Hub was one of them.

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Jacques Pütz, CEO of LUXHUB was one of them.

With a strong team, Morgan Wirtz is building Rise, a neobank for teens to lift financial education to help them better manage their finances and reduce financial stress

EBRC and The Banking Scene joined forces to interview key stakeholders from Luxembourg’s FinTech and banking industry. Alexandre Castaing of RBC was one of them.

Loading more...

With a long history in purposeful banking, we invited their chairwomen to talk about how they look at banking for good today

How important are bank Fintech Partnerships in payments and how to achieve great partnerships? We spoke with Banking Circle, BNP Paribas and PayBelgium

Is it time to talk more about the banking creations with impact instead of purely looking at technological advancement in fintech?

Automation , RPA and and more intelligent ML solution can help banks grow employee engagement and customer inclusion

David Bohn of MyBudget was our guest to talk about financial wellbeing and their business in Australia to get society financially fitter

In the light of the second anniversary of PSD2s RTS, we discussed the state of open banking in B2B with Isabel Group and ABN AMRO

How can automation and RPA contribute on both strategic and tactical level to bank's ESG ambitions? We spoke to Chris Skinner, PwC, UiPath and NatWest

The open banking journey of Deutsche Bank started in 2015 with de development of an API Program. Joris Hensen shared their lessons learned

The Unexplored Territory of Gaming for Banks: an introduction in platformication and gamification of banking and bankification of gaming

Banks struggle to apply the vision and ambitions they have to improve and grow their contributions to a greener and better society, how can automation help?

What are the challenges ahead before banks embrace crypto assets and NFTs as part of their value proposition, and how could this look like?

ABN AMRO Belgium is supporting many initiatives for a greener, EGS-friendly future, and this is how they accelerate the sustainable shift in Belgium

With PayBelgium and Emerging Payments Association we investigate their contributions to innovations in payments

Like Heracles changed the rules to clean the Augean stable, the banking and fintech industry need to reinvent their approach to financial wellbeing.

Green mortgages for sustainable living is more than a label. With a direct impact on a bank's (future) financial results, acting now is imperative for the industry

Loading more...

With the rise of RPA-based attended bots we are getting closer to a bot for every employee. What is required to make this a reality?

With PSD2 and open banking to stimulate innovation, EPI and the digital euro (CBDC) are told to create more uniformity across Europe

We all know the struggles of a partnership between banks and fintech companies, but what are the remedies?

As automation tools in banking get smarter, evolving from RPA to intelligent automation, bots evolve from being a virtual assistant to a genuine colleague

The human factors behind automation at ING and NIBC Bank: employee engagement, customer experience and cost avoidance

It is time to rethink digital banking, to align it to customer expectations and to make it more human again in a connected way.

Innovations in cards and payments are endless these days, and retail banks will need to make strategic dilemmas to deal with them.

How more data points end up with more creative credit scoring models to enhance financial inclusion in developing regions like Asia and Africa

On April 15 we discussed with Peter Theunis of Radar Payments what is shaking the cards and payments industry, find the most relevant insights in this blog

Automation in Banking success does not depend on technology, but the leaders that drive a cultural change to embrace automation as a part of the job

Automation in Banking to setup control mechanisms to find and fix errors in banking processes, improve data quality of central functions and augment the value of employees

With Véronique Léonard, CFO we spoke how Bank J. Van Breda & C° are looking at banking for good, purposeful banking and sustainability and ESG

Don't make your RPA project a cost-cutter. This blog identified a couple of concrete, measurable results how RPA improved the business of a bank

With Marc Lauwers, CEO of Argenta, we discussed what purpose and sustainability means to them and how they contribute to a better future for human and society

Loading more...

SME Banking will never be the same again: COVID-19 accelerated the need for digital banking and more specifically for SMEs

How can wealth managers provide their clients with comprehensive data and analytics through a broad mix of digital channels, so they can make more informed investment decisions?

What must change for banks to become true financial advisors, doctors of a customer's financial health?

Everyone talks about automation in banking, but what do bankers really know about automation, RPA and intelligent automation, where do they see the gains and opportunities?

With YTS (Yolt Technology Services), we investigated the possibilities of PSD2, Open banking and open finance to turn it into a remedy for people and businesses to recover from COVID-19

With Karel Baert, CEO and Claire Godding, Head of Diversity and Inclusion at Febelfin, Belgian Federation of banks, we discussed what "Banking for Good" means to them

Find out what executives from Spotify, State Street Bank and DFCG, the French Centre of CFOs thought us of how to make your RPA, automation and intelligent automation projects a success

We used an innovative interview method called the ‘portable kit study’ that involved asking people to take everything out of their bags and wallets and talk us through what they carry with them on a daily basis, cash, cards

We invited Hedwige Nuyens, Managing Director of IBF to talk about the bank of the future, where we spoke about COVID-19, digital, branches, BigTech, CBDC, crypto, the role of savings and community banks and much more

Erin B. Taylor provides a couple of useful tools that can help to better understand how consumers feel and think about, and act with money

Together with Peter Theunis of Radar Payments and BPC Banking Technologies and Jeroen de Bel of Fincog, we investigated how digital banking changed and what their future holds

We spoke with Thomas Courtois, CEO of neobank Nickel about Financial Inclusion and he shared us what this means to them and how they achieve this by living to their values: universality, simplicity, utility and benevolence

Aion surveyed over 1,000 Belgians and found that over 75% of Belgians of all ages feel it’s important to be financially prepared, but more than 50% said that they didn’t feel sufficiently prepared for the future.

What were the most popular opinions on The Banking Scene's website?

Predicting 2021 with Chris Skinner: How will economy evolve, and fintechs and banks? What to expect from challenger banks and what is key to make them more relevant?

Loading more...

Monster and Myths of Innovation are everywhere, in all industries. The last session of The Banking Scene Afterwork was a conversation about those monsters and how to cope with it.

We discuss what open finance is, what its impact is for financial services, where the low-hanging fruit is and how to grasp these opportunities

The Banking Scene spoke to Axel Weiss, Head of Payments at the German Savings Bank Association (DSGV) about the latest trends in payments and the impact of ’SWIFT’s new strategy for their members

We invited David Versteeg, Chief Digital Officer at van Lanschot Kempen to share us their digital transformation journey

Kate is KBC's digital assistant that will personally and proactively assist customers in making their financial life easier, through AI, automation and personalisation

Hyperautomation - an answer to automate more complex customer and employee journeys of a bank by combining RPA, Machine Learning and other AI techniques

6 Lessons from Customer Experience (CX) with clear examples of the banking industry and more specifically in B2B

Founded in 1973, SWIFT is the one the connects the dots in financial services. What is their new strategy and collaboration model for banks?

Will video banking be the new way for banks to engage with customers? We spoke with Klaas Ariaans, Managing Director Personal Banking at ABN AMRO Bank

Learn how Hyperautomation can grow the business of Microfinance Institutions while increasing customer experience with a mix of RPA and Machine Learning - UiPath

What can we learn from Minna Technologies and ING in the way they partner? A fintech and a bank about the importance of communication and expectation management

Read my thought on personalized banking, after reading Comarch' white paper, called "Personalization of Banking Services via Digital Transformation"

What can conventional banking learn from Islamic banking and what is the future of Islamic banking and Islamic fintech? We spoke with Wajeeha H. Awadh of Al Baraka Banking Group

Loading more...

What does it mean for a bank to be open? What value will it bring to this bank and its customers? How did the industry do thus far?

One-size-fits-all is over: we need financial services innovation for women. They think differently about money, they talk different about it and they act different.

Key conclusions from a discussion with Jo Vercammen the state of crypto, cbcd, central bank digital currency and blockchain and how it affect the banking industry

Prices in the banking industry are not always very transparent. Belgian's newest bank, Aion, countered this by setting a business model based on a membership.

Our conversation with 2 experts of UiPath, Guy Kirkwood and Amit Kumar demonstrated that automation and RPA are making the banking industry more human on multiple fronts

Read my lessons from The Banking Scene Summer Event on Banks Doing Digital, with Chris Skinner (thefinanser.com), Benoit Legrand (ING) and Karin van Hoecke (KBC)

For many entrepreneurs, microlending is vital to the required financial inclusion to set up a business. In Belgium, the company microStart gets support in microfinance by Accenture and BNP Paribas Fortis

June 11 was a good day! Jan van Vonno, Research Director at Tink was our special guest at The Banking Scene Afterwork to answer all the questions I had on their recent study, titled: 'the investments and returns of open banking'.

Make sure Operational Resilience is on top of your agenda, whether you work in a bank, or a fintech, in risk or sales, compliance or IT

A bank must support its customers in having a financially balanced life, helping them to reduce financial stress by improving their financial wellbeing.

Bank branches are not dead, but how can they get most value out of that, at a low cost? Post COVID this question is even more pressing than in 2019

How has COVID-19 affected the way banks start new fintech relationships? Today people are going back to their old reflexes. Today they go back to the companies close to them, it takes longer to have a relationship and they require more effort in trust between the involved organisations.

The SME banking segment is booming business in the fintech industry for years. COVID will accelerate this process for multiple reason, here is why

COVID-19 changed the way the banking industry worked. What will be the long-term impact? The key messages of The Banking Scene Afterwork 23 April with special guest Guy Claes

Loading more...

COVID-19 is the biggest remote working Proof Of Concept… ever! Everyone needs to rethink how they work, shop and live. From one day to the next, we are all living in a completely new context, with new needs and different problems to manage and also with great new ideas to anticipate those needs and problems.

What will be the longterm impact of COVID-19 on the way we pay in Belgium, Netherlands and Luxembourg? From contactless to no contact, biometrics and instant

How COVID-19 changed our perception on cash, contactless, and short-term also on innovation in payments

Who will be the winners and losers of this crisis in the financial technology industry, why this crisis is fundamentally different from the one in 2008, and why China will take a fundamentally different approach to resolve the economic crisis in the period to come.

A talk with Jo Caudron, about the societal transformation in the coming 10 years and the impact on the banking industry

Koen Vanderhoydonk chaired our conference #TBSCONF20LUX, on January 30th in Luxembourg. You probably remember this was about trust, the central theme of The Banking Scene this year.

At the launch of a new challenger bank in Belgium, Aion, The Banking Scene had the chance to interview their CCO Wojciech Sass

6 learning from the panel I moderated at Finovate: “Successes & Challenges Faced Since We Went Live With Open Banking”

Brian Bushnell, shares his insights on how banks can become more TRUSTED by mutualizing services at #TBSCONF20LUX

A78 is built to facilitate communication between fintech and banks in the context of PSD2

Looking back at The Banking Scene 2020 Luxembourg: after movie #TBSCONF20LUX

How is N26 looking at trust? How did the lack of trust in banks helped them in building trust for their customers, today and in the future?

Loading more...

Trust in financial services is changing. Where does this change come from, what is the impact? Based on Rachel Botsman's "Who can you trust?"

Open Banking and PSD2: an evaluation by Belfius' Director of Product Management Payments and Credit Arnaud Delputz

The past decade provided a wave of new technologies with tremendous opportunities, the coming years, the banking industry will start to understand how to use it for more human banking

The future of Instant Payments and Cards - The Round Table Sessions (December 3rd) by The Banking Scene, a testimonial by Inna Kostiuk

The Open Banking Interviews with Nathalie Knops, Head of Business Transformation at Banque Internationale à Luxembourg (BIL)

The Open Banking Interviews with Tjeerd Tesselaar, Area Lead Product Development & Partner Management and Nico Strauss, Tride Lead B2B Services at Rabobank

Frictionless and biometric payments require a consumer to allow you in his inner circle. How far can you go? A few examples

The Open Banking Interviews with Marc Lauwers, CEO and Inge Ampe, CCO of Argenta on their views on Open Banking, PSD2 and how it impacts Argenta's business model

Mortgage loans are the new battlefield for innovation. Why is it so hard to innovate in this business line?

A blog about the rise of Instant Mortgage, Open Mortgage, and the quest for the best customer journey to look for a real estate property

The Open Banking Interviews with Karel Van Eetvelt, CEO, Febelfin

The biggest impact of PSD2 for corporates will be in the new way services providers think of financial services in the near future and how they will provide it to the end-customer.

Read what Jasper Nienhuijs, Head of Market Management at de Volksbank thinks about PSD2 and Open Banking

The Open Banking Interviews: Wajeeha Hussain Awadh, Section Head of Digital Banking & Fintech, Al Baraka Banking Group

Loading more...

Did something revolutionary happen? Did PSD2 hit the headlines? Were consumers quickly adapting their financial behavior? Was there the so long predicted shake-up of the market? Did banks go bankrupt because fintech and Bigtech took over?

The Open Banking Interviews with Laurent Dumont, Digital Banking Manager and Kris Roggeman, Squad Leader Open Banking at Crelan

The Open Banking Interviews, with Maarten Verboven, Director of Open Banking at BNP Paribas Fortis

What role does Visa play in the game of invisible and frictionless payments? And how do they support keeping customers in control of consumption?

Open Banking Interview with Fanny Solany, Head of Digital, Retail & Markets Regulation, CaixaBank

Open Banking Interview with Ali Niknam, CEO of bunq Bank

Non-bank players are looking for new market in the banking space: Immoweb wants to go into mortgage loans

The Open Banking Interviews with Raphael d'Ostuni, Head of Open Banking and Partnerships at Keytrade Bank

How does Starling Bank look at Open Banking and PSD2? Read about it in this episode of the Open Banking Interviews with Helen Bierton, Head of Banking, Starling Bank

Rabobank showed the intention to take over Eneco? What is behind this move? How are banks increasing their societal relevance with this potential takeover?

How does KBC look at PSD2 and Open Banking? We talked about this with Karin Van Hoecke, General Manager Digital Transformation, KBC Bank & Insurance Belgium

ATMs and cash remain a hot topic in discussing banking and financial services in Belgium. What would be the reason that supermarkets are hesitant to invest in their own ATMs?

ABN AMRO is betting high on APIs, how do they think about Open Banking and PSD2? Read all about it in our conversation with Koen Adolfs, Product Owner & API Evangelist, ABN AMRO Bank

Open Banking is only possible with an open mindset. If the technology is not a succes of that, it will not work

Loading more...

The Open Banking Interviews: Daniel Van Delft, Country Manager Visa, Netherlands

Deutsche Bank has an API Platform and they were eager to share more about it with The Banking Scene in an interview with Joris Hensen, Founder and Co-Lead of their API Program

Money 20/20 Europe report by The Banking Scene: what are a bank's key threats today?

Inna went to Money 20/20 with Fintech Belgium and left her testomial for The Banking Scene and all that wish to read it

Inna attended The Banking Scene Conference (#tbsconf19) and shared her impressions with us

Fintech and banks is all about collaboration these days thanks to open banking etc... what makes a great collaboration?

Lies Van Hemerlijck represented The Banking Scene at Know Conference 2019 and she was happy to share her take aways

Innovation in Payments, what is it all about?

Apple launched it AppleCard, a new feature in the Apple ecosystem. It is really about payments? Or should we look in the direction of identity?

The Banking Scene attended Money 2020 Asia. What were the key takeaways from this highly valued conference?

The future of banking will be determined by PSD2 and Open Banking. How will banking look like in the future?

How can banks grow their relevance for society? Some banks already start thinking out of the box.

Loading more...

Bigtech keep growing and they keep trying to get hold on financial services. Will they succeed?

15 years to rediscuss the gentlemen’s agreement on 24 free cash withdrawals

As banks start adopting instant payments, the quest for additional revenuew through this new payment means remains complicated

An explanation of ontology-centric banking, semantic banking

Rik Coeckelbergs participated in the test period of KBC wearables, contactless payments. Read his testimonial here

Revolut has a banking licence, what does this mean for the banking industry? And why did they go to Lithuania for this?

Revolut hired a country manager for Belgium, what does this mean in terms of their local ambitions?

Open Banking will change the way we bank, not just the way we pay

Contactless is still perceived as unsafe, yet statistic show another view. What are the myths behind this?

As society evolves from less cash to cashless, national banks start to react

Where is Belgium today in term of mobile and contactless payments? What is the impact on cash usage?