Insights & Opinions

Bank of the Future: From Mobile First to Open First?

Tue, 09 Mar 2021

Peter van Hees, co-founder and Head of Product at Cake and former innovation manager at KBC Bank has never been afraid of sharing visions on the future. According to him, the bank of the future is mission-driven, invisible and pro-active.

The one-hour discussion on March 4 ended up with many open questions and even more visionary ideas on the future of banking. The highlight, in my view, was the question of whether banks can truly fulfil the mission of being invisible and pro-active if they remain loyal to a mobile-first strategy.

The first time I met Peter, about five years ago, Belgian banks were in the middle of getting their mobile apps in order. Mobile was the future. Back then, Peter witnessed the first fear of big tech entering banking. Cloud, data and artificial intelligence were told to transform the industry by 2020.

Banking apps are great today, but what comes next?

Evaluating these trends today, Peter observes that banks did well with their mobile apps: “The overall quality of apps has drastically improved. Today, you stand out if you have a banking app that doesn’t work. The user experience is a little bit everywhere.”

Mobile is the dominant channel today, but Peter is already looking forward. New technologies will arise, and they will hopefully solve part of the customer pains coming from mobile-first strategies, the biggest one being the pull mechanism behind a mobile-first approach.

Whether it is alerts and notifications, transaction data, marketplaces, all these developments have one goal: pulling in the customer’s attention.

Peter: “I don’t know what comes next, but we will move to a technology that makes us smarter, Instead of just providing us, I would say all the information in our pockets. This new technology will provide us with that smartness, the right insights at the right time in the right context, based on your behaviour.”

It will be a channel on top of mobile, and banks need to get ready for this next transformation.

Plenty of data, little proactive insights

According to Peter, the banks that seized the data opportunity used it predominantly to sell more products instead of improving the customer’s financial well-being and the customer experience, which is a missed opportunity.

Peter: “For me, in terms of user experience, you can provide an excellent app with nice screens. But ultimately, user experience is tied to intelligence. And basically, you’re catering up for different types of profiles, from the accountant on one end to a surfer on the other end, who doesn’t care about all the exact numbers.”

Banks will need to look further than pure transactional data to achieve intelligent insights. They need to look further than the data they manage to understand a customer’s personal information at a much more granular level, ultimately helping them understand each individual’s needs.

The most demanded feature of Cake is not the rewards or the cashback, according to Peter. It is insightfulness. Why can’t banks provide the same insights?

“Of course, they can. But they don’t have to. There might be a conflict of interest in some areas, which consumers are well aware of. I don’t see the bank working together with CEBUD (Centre for Budget Advisory and Research), for example, to provide a framework,” said Peter. “I think it’s the bank will basically set the parameters of CEBUD and say, you can look into this, this and this, but don’t try to optimise either your mortgage or so on. Our business model of data monetisation is not based on selling financial products.”

You cannot talk about data without talking about PSD2 and open banking. The regulator did an excellent job forcing banks to open up. Unfortunately, the success is limited in countries, like Belgium.

Peter blames a lack of educating consumers on PSD2: “In the Netherlands, the government was late to implement in the banks; they caught up quite quickly, and they very quickly started to educate the market about it. Belgium started sooner, but there was no education of the market whatsoever for PSD2, and still not today.”

If consumers don’t know it, they will not use it. It slows down open banking adoption by the market. That is unfortunate, and it risks to become a missed opportunity, as it probably is only the start of a long evolution to an open data society.

The open data society is an immense opportunity soon for banks that wish to provide more proactive services with value-creating insights for the customer, bringing banking many steps closer to what Karin van Hoecke once called “the ultimate laziness for the customer”. To succeed, consumers will need to trust data sharing technologies, and this requires education.

“I think this ultimate laziness is a very simple quote. Imagine my partner and me: that relationship has built up over the years. To get to ultimate laziness, you need much information, need context, and behaviour,” Peter explained. “If I come home from a hard day at work, the ultimate laziness will not be lying on my couch. It might be to cook dinner because that relaxes me. So you need many elements before you can achieve this proactive service. And provide it. Could banks do it? Of course, but it’s a focal point.”

It is not essential to a bank’s services offering today in his opinion.

What banks can learn from the evolution to invisible payments

We don’t know what the next banking channel will be, but the payments industry gives a few exciting indications into that direction.

Perhaps the next channel will not be a banking channel at all.

When talking about invisible payments, Peter refers to the experiences of OPnGO, Tesla charging and Amazon Go, where you get what you need, and the payment is pushed to the back, making it invisible for the consumer.

Peter: “I frequently pay without looking at the bill. So you can say that that payment is more or less invisible to me. Why do I even need to scan my phone and pay? I prefer to walk out, and at the end of the month, I’ll look at my stats and see if I spend more or less on my groceries.”

We are almost there, but to make it completely invisible, the industry only needs to remove the friction of getting the phone and making a contactless mobile payment. In this evolution, Peter believes that banks have a facilitating role but no longer a leading role.

“I’ll have a look in the evening or two days later. So what I want is what I call the KYS (Know Your Spending) or KYP (Know Your Payments). I think banks need to provide better insights than they’re doing today on showing you what you paid for, as these transactions can be quite cryptic. Banks have a role to play in changing their old-fashioned way of simply showing transactions with very obscure descriptions.”

In Peter’s vision, the invisible bank is a bank without a front-end channel. “My future bank doesn’t exist yet: a real bank that has only an open banking strategy,” explained Peter. “A bank that doesn’t focus on their own mobile apps, which plugs into whatever front-end or service or customer journey.”

One of the barriers to this future is another conflict of interest: the loss of distribution and a proprietary communication channel, meaning they lose the customer locking opportunity of their mobile banking app. Which banks is the first to be prepared to lose this customer contact in favour of customer delight?

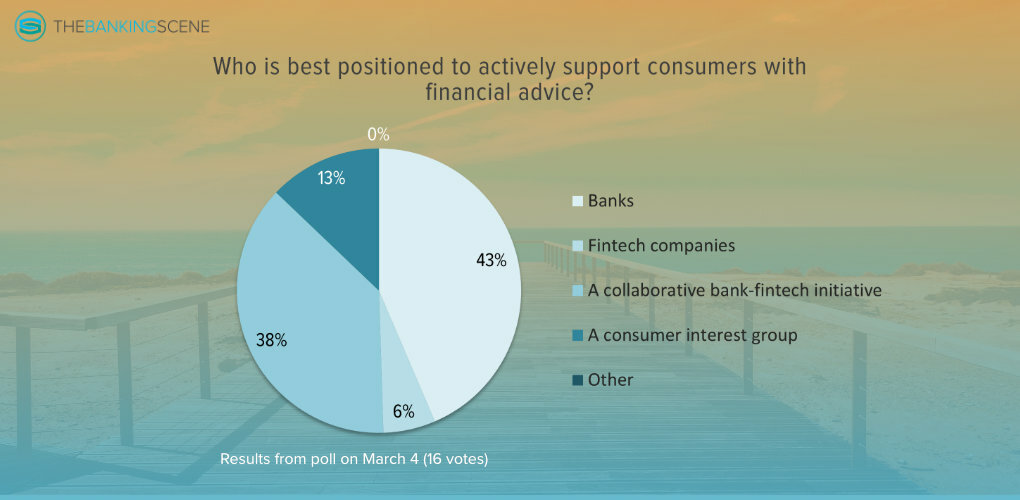

Is invisible banking enough to create the ultimate, independent, proactive banking experience?

Suppose the industry can overcome the barrier of losing customer contact: will banks provide an authentic, independent, proactive banking experience?

It depends on whom you ask. Many banking executives joined The Banking Scene Afterwork before saying that banks have a role to play as financial doctors for their customers. They were convinced that banks must look at the long-term relationship.

Peter and a few people from the audience saw this differently. They believed that the purpose of a bank today is balancing too hard towards “earning money”, making independent, proactive banking experience a utopia. They don’t believe a bank will ever advise a customer to switch a mortgage loan to another bank if that customer would be better off there.

That is what people would expect from a financial doctor who gets access to all possible and relevant data to make a consumer financially fitter. This barrier makes independent third-parties better positioned to become financial doctor, according to these people.

Someone suggested a company to remove ALL the friction of financial services. Through AI, this company would not only list the relevant products for a customer but also select the best possible product on the market. Their customers may not be switching banks for the best possible service, but they will change products whenever this would make the customer better.

Conclusion

You can call me naïve, but if you ask me, I do believe that banks can become financial doctors, but it will take guts to shift from product offering to services offering. It is an old debate, and thus far we have not seen many examples in that direction, but I remain hopeful.

By inviting Peter, we got a fresh view on the possible future bank, with many questions unanswered. As the industry evolves, some of these questions will be answered or made redundant. What is certain is that this session gave a lot of food for thought for both banks and for The Banking Scene Afterwork, with plenty of inspiration for future sessions.