Insights & Opinions

The rise of superapps in ASEAN at Money2020 Asia

Sun, 24 Mar 2019

Last week was the second edition of Money20/20 Asia in Singapore. The conference was once again the perfect place to gain a better understanding of the dynamics in ASEAN financial services industry.

Like last year, the conference was quite an eye-opener from time to time. This post will run you through the remarkable phenomenon of the rise of superapps.

It all started with a prepaid payments model…

In a region with a lot of islands and a high percentage of unbanked many new Fintech companies rose up last year at Money20/20 Asia with payments services. Grab was one of the examples last year, BigPay was another. Both companies started in the transport business and saw payments as a logical next step in their expansion for better services to existing customers and as an access point for new customers. Grab started as a car hailing platform, BigPay is a spin-off of AirAsia. These players were present this year again, to demonstrate their new functionalities. A lot of similar companies showcased as well.

Many mirrored themselves to the situation in China, with WeChat as a front-runner in the superapp business. Apparently people just like to have one app for all different functionalities in Asia.

… and it quickly shifted to a complete commerce platform…

Take OVO, the “one wallet for all in Indonesia”. Jason Thompson, CEO of the platform, provided a very interesting introduction in their model.

Aside from being a payments platform, they developed into e-commerce, they integrated Grab Card, GrabFood, merchant acquiring, insurance, telco services... They got into a situation where a consumer gets in touch with them for almost everything. Can you imagine the value they generate, simply by making smart use of the data they collect? To give you an idea of their size: 150 million devices are equipped with at least 1 app that is connected to OVO services.

OVO is, like so many other superapps, built on a segment of consumers without, or with limited access to banks. Indonesia has a staggering number of 60% under- or unbanked consumers. Less than 10% has access to loans and investment penetration is only 0,3%. Despite these numbers, the country has 60 million small businesses, often without any access to financial services.

Why are banks not really interested? Well, the average amount of top-ups on their accounts is 18 dollar. For many of you this may sound irrelevant. That is also how many of these local banks think about 18 dollar.

They all underestimate the importance of 18 dollars though. Keep in mind that in countries like Indonesia, this small number is a matter of survival. 18 dollars is an equivalent of 18 meals for the local community.

So with a modern, low cost infrastructure 18 dollars becomes a huge opportunity. Since it is a prepaid model, they build on more flexible regulation. That helps them to keep their processes of onboarding and KYC very lean. On top of that it is an unserved market, eager to participate in the regular economy.

To give you an idea of the loyalty they get from their users: last year OVO distributed 600 million loyalty points, and 95% were redeemed! How many can say that of their own programs?

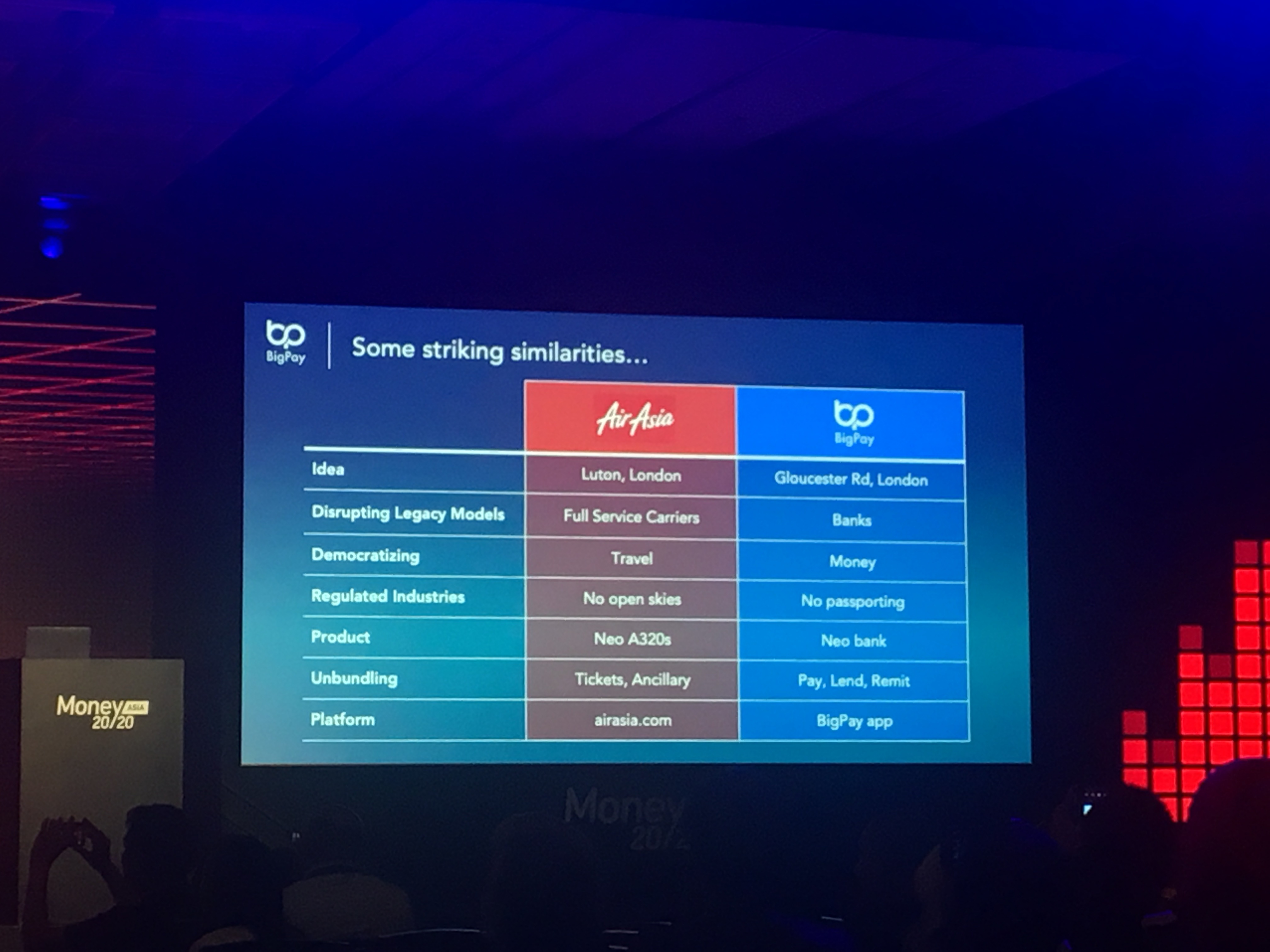

The same goes with BigPay, the financial services brand of Asia Air. In 1 year time they there the 5th biggest downloaded app in Malaysia. Today they have a decent app that facilitates payments, tomorrow they have their licence for the high volume remittance business, and for lending.

With all the islands, the many countries, currencies and migrant workers, the remittance opportunities are huge. Having a low-cost platform is essential here. The value of transactions is low, and you need to outperform the incumbents in price. This is where blockchain has a huge potential.

… and it is extending now to a complete micro financial services offering

THE eyeopener for me at last year’s conference was Grab. They became a big player thanks to the acquisition of Uber in South-East Asia. Going from chat to multiple payments products, they provided a real platform of services, all to provide more value to their customers.

This year they were present again to demonstrate their new services. One of the topics was the extension to insurance products. It took them 3 months from signing the contract with a partner to the launch of the insurance offering. They collaborate with Chinese Zhongan, a Chinese insurance company. Zhongan does the production, Grab takes care of the distribution.

They also announced the extension of their offering to a whole set of new services to help their SME partners to grow further. “Grow with Grab”.

The bottom line idea is that if they let their SME partners grow, they will also end up better. The program is based on 3 pillars:

- Generate more earnings with new payment technologies

- Grow your business with micro loans

- Gain peace of mind with micro insurance

These SMEs are often too small to be a relevant bank customer today. Micro insurance and micro loans can be a huge difference for SMEs, but banks are not interested in providing it. On top of that, the mobile revolution opens a lot of doors for these self-made men and women, especially with the access to the superapp platforms: for the first time they can promote an sell their products and services online.

“Grow by Grab” can become a serious challenge on the long run for banks: today they attract customers with an irrelevant size from banks, but what will happen when they grow? Will they be interested to return to the bank, or will they maintain their relationship with Grab?

Micro products require less regulation, but if Grab plays it well, they could become a serious threat on the long run. Like Douglas Faegin, President of International Business of Group Ant Financial said: “It is easier to start with a simple onboarding process and to nurture extra customer data later on, than having a complex onboarding from the beginning.” It starts with mobile top-up, but once integrations with financial services providers are possible, the opportunities become endless, like also the use cases OVO and Grab showed.

Will banks be ready to provide an answer?

Banks start to realise the threat, or let’s say: they start to understand the huge opportunity of an increasingly larger amount of potential customers. Many consumers and SMEs grew their footprint thanks to the products offered by these new players.

Software companies, like the Chinese Hundsun try to help banks to become leaner, and to become ‘a superapp’. Their CEO, Angela Carcheska, see superapp as nothing more than “a streamlined data flow that allows to connect with external provider” (sounds more like Open Banking to me, but OK). She is convinced that by migrating banks to a cloud-based microservices platform, they take already a huge step in the right direction.

Question is whether the banks’ answer will be enough. Creating a superapp is to much more than modernising a core banking infrastructure. It is sometimes more a matter of marketing than of technology. What will be their story, their answer to the rising stars?

These rising stars start from nothing to everything. It is a lot harder to go from everything to something more. That is, I think, exactly the challenge that banks will be facing if they wish to become a true superapp in Asia.

Today banks still have the regulator at their side. Tomorrow there is no reason why the new players would not apply for a banking license to become a full financial services providers.